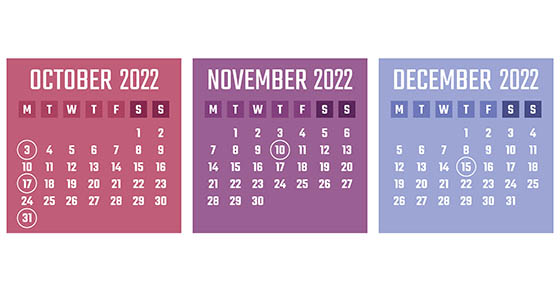

Here are some of the key tax-related deadlines affecting businesses and other employers during the fourth quarter of 2022. Keep in mind that this list isn’t all-inclusive, so there may be additional deadlines that apply to you. Contact us to ensure you’re meeting all applicable deadlines and to learn more about the filing requirements.

Note: Certain tax-filing and tax-payment deadlines may be postponed for taxpayers who reside in or have businesses in federally declared disaster areas.

Continue Reading

As a result of the current estate tax exemption amount ($12.06 million in 2022), many estates no longer need to be concerned with federal estate tax. Before 2011, a much smaller amount resulted in estate plans attempting to avoid it. But now, because many estates won’t be subject to estate tax, more planning can be devoted to saving income taxes for your heirs.

While saving both income and transfer taxes has always been a goal of estate planning, it was more difficult to succeed at both when the estate and gift tax exemption level was much lower. Here are three considerations.

Continue Reading

In its latest report, the National Association of Realtors (NAR) announced that July 2022 existing home sales were down but prices were up nationwide, compared with last year. “The ongoing sales decline reflects the impact of the mortgage rate peak of 6% in early June,” said NAR Chief Economist Lawrence Yun. However, he added that “home sales may soon stabilize since mortgage rates have fallen to near 5%, thereby giving an additional boost of purchasing power to home buyers.”

If you’re buying a home, or you just bought one, you may wonder if you can deduct mortgage points paid on your behalf by the seller. The answer is “yes,” subject to some important limitations described below.

Continue Reading

High-income taxpayers face two special taxes — a 3.8% net investment income tax (NIIT) and a 0.9% additional Medicare tax on wage and self-employment income. Here’s an overview of the taxes and what they may mean for you.

3.8% NIIT

This tax applies, in addition to income tax, on your net investment income. The NIIT only affects taxpayers with adjusted gross income (AGI) exceeding $250,000 for joint filers, $200,000 for single taxpayers and heads of household, and $125,000 for married individuals filing separately.

Continue Reading

Do you own a successful small business with no employees and want to set up a retirement plan? Or do you want to upgrade from a SIMPLE IRA or Simplified Employee Pension (SEP) plan? Consider a solo 401(k) if you have healthy self-employment income and want to contribute substantial amounts to a retirement nest egg.

This strategy is geared toward self-employed individuals including sole proprietors, owners of single-member limited liability companies and other one-person businesses.

Continue Reading

If you’re a business owner working from home or an entrepreneur with a home-based side gig, you may qualify for valuable home office deductions.

But not everyone who works from home gets the tax break. Employees who work remotely can’t deduct home office expenses under current federal tax law.

Continue Reading

When a married couple files a joint tax return, each spouse is “jointly and severally” liable for the full amount of tax on the couple’s combined income. Therefore, the IRS can come after either spouse to collect the entire tax — not just the part that’s attributed to one spouse or the other. This includes any tax deficiency that the IRS assesses after an audit, as well as any penalties and interest. (However, the civil fraud penalty can be imposed only on spouses who’ve actually committed fraud.)

Innocent Spouse Relief

In some cases, spouses are eligible for “innocent spouse relief.” This generally involves individuals who were unaware of a tax understatement that was attributable to the other spouse.

Continue Reading

The business entity you choose can affect your taxes, your personal liability and other issues. A limited liability company (LLC) is somewhat of a hybrid entity in that it can be structured to resemble a corporation for owner liability purposes and a partnership for federal tax purposes. This duality may provide you with the best of both worlds.

Like the shareholders of a corporation, the owners of an LLC (called “members” rather than shareholders or partners) generally aren’t liable for business debts except to the extent of their investment. Thus, they can operate the business with the security of knowing that their personal assets are protected from the entity’s creditors. This protection is far greater than that afforded by partnerships. In a partnership, the general partners are personally liable for the debts of the business. Even limited partners, if they actively participate in managing the business, can have personal liability.

Continue Reading

Although merger and acquisition activity has been down in 2022, according to various reports, there are still companies being bought and sold. If your business is considering merging with or acquiring another business, it’s important to understand how the transaction will be taxed under current law.

Stocks vs. Assets

From a tax standpoint, a transaction can basically be structured in two ways:

Continue Reading

If you’ve recently begun receiving disability income, you may wonder how it’s taxed. The answer is: It depends.

The key issue is: Who paid for the benefit? If the income is paid directly to you by your employer, it’s taxable to you just as your ordinary salary would be. (Taxable benefits are also subject to federal income tax withholding. However, depending on the employer’s disability plan, in some cases they aren’t subject to Social Security tax.)

Continue Reading

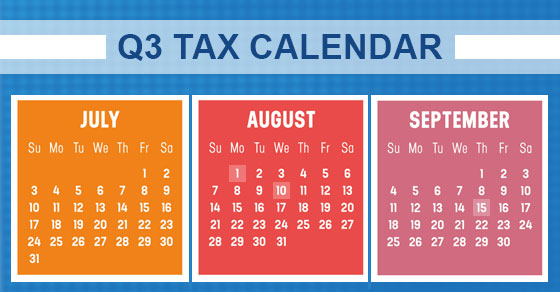

Here are some of the key tax-related deadlines affecting businesses and other employers during the third quarter of 2022. Keep in mind that this list isn’t all-inclusive, so there may be additional deadlines that apply to you. Contact us to ensure you’re meeting all applicable deadlines and to learn more about the filing requirements.

Continue Reading

Are you in the early stages of divorce? In addition to the tough personal issues that you’re dealing with, several tax concerns need to be addressed to ensure that taxes are kept to a minimum and that important tax-related decisions are properly made. Here are five issues to consider if you’re in the process of getting a divorce.

- Alimony or support payments. For alimony under divorce or separation agreements that are executed after 2018, there’s no deduction for alimony and separation support payments for the spouse making them. And the alimony payments aren’t included in the gross income of the spouse receiving them. (The rules are different for divorce or separation agreements executed before 2019.)

Continue Reading

As a result of the current estate tax exemption amount ($12.06 million in 2022), many people no longer need to be concerned with federal estate tax. Before 2011, a much smaller amount resulted in estate plans attempting to avoid it. Now, because many estates won’t be subject to estate tax, more planning can be devoted to saving income taxes for your heirs.

Note: The federal estate tax exclusion amount is scheduled to sunset at the end of 2025. Beginning on January 1, 2026, the amount is due to be reduced to $5 million, adjusted for inflation. Of course, Congress could act to extend the higher amount or institute a new amount.

Continue Reading

The downturn in the stock market may have caused the value of your retirement account to decrease. But if you have a traditional IRA, this decline may provide a valuable opportunity: It may allow you to convert your traditional IRA to a Roth IRA at a lower tax cost.

Traditional vs. Roth

Here’s what makes a traditional IRA different from a Roth IRA:

Continue Reading

The IRS recently released guidance providing the 2023 inflation-adjusted amounts for Health Savings Accounts (HSAs). High inflation rates will result in next year’s amounts being increased more than they have been in recent years.

HSA Basics

An HSA is a trust created or organized exclusively for the purpose of paying the “qualified medical expenses” of an “account beneficiary.” An HSA can only be established for the benefit of an “eligible individual” who is covered under a “high deductible health plan.” In addition, a participant can’t be enrolled in Medicare or have other health coverage (exceptions include dental, vision, long-term care, accident and specific disease insurance).

Continue Reading

Taking care of an elderly parent or grandparent may provide more than just personal satisfaction. You could also be eligible for tax breaks. Here’s a rundown of some of them.

Continue Reading

Are you a charitably minded individual who is also taking distributions from a traditional IRA? You may want to consider the tax advantages of making a cash donation to an IRS-approved charity out of your IRA.

When distributions are taken directly out of traditional IRAs, federal income tax of up to 37% in 2022 will have to be paid. State income taxes may also be owed.

Continue Reading

If you donate valuable items to charity, you may be required to get an appraisal. The IRS requires donors and charitable organizations to supply certain information to prove their right to deduct charitable contributions. If you donate an item of property (or a group of similar items) worth more than $5,000, certain appraisal requirements apply. You must:

- Get a “qualified appraisal,”

- Receive the qualified appraisal before your tax return is due,

- Attach an “appraisal summary” to the first tax return on which the deduction is claimed,

- Include other information with the return, and

- Maintain certain records.

Keep these definitions in mind. A qualified appraisal is a complex and detailed document. It must be prepared and signed by a qualified appraiser. An appraisal summary is a summary of a qualified appraisal made on Form 8283 and attached to the donor’s return.

Continue Reading

The IRS has begun mailing notices to businesses, financial institutions and other payers that filed certain returns with information that doesn’t match the agency’s records.

These CP2100 and CP2100A notices are sent by the IRS twice a year to payers who filed information returns that are missing a Taxpayer Identification Number (TIN), have an incorrect name or have a combination of both.

Continue Reading

In some cases, homeowners decide to move to new residences, but keep their present homes and rent them out. If you’re thinking of doing this, you’re probably aware of the financial risks and rewards. However, you also should know that renting out your home carries potential tax benefits and pitfalls.

You’re generally treated as a regular real estate landlord once you begin renting your home. That means you must report rental income on your tax return, but also are entitled to offsetting landlord deductions for the money you spend on utilities, operating expenses, incidental repairs and maintenance (for example, fixing a leak in the roof). Additionally, you can claim depreciation deductions for the home. You can fully offset rental income with otherwise allowable landlord deductions.

Continue Reading

What are the tax consequences of selling property used in your trade or business?

There are many rules that can potentially apply to the sale of business property. Thus, to simplify discussion, let’s assume that the property you want to sell is land or depreciable property used in your business, and has been held by you for more than a year. (There are different rules for property held primarily for sale to customers in the ordinary course of business; intellectual property; low-income housing; property that involves farming or livestock; and other types of property.)

Continue Reading

Like many people, you may have dreamed of turning a hobby into a regular business. You won’t have any tax headaches if your new business is profitable. But what if the new enterprise consistently generates losses (your deductions exceed income) and you claim them on your tax return? You can generally deduct losses for expenses incurred in a bona fide business. However, the IRS may step in and say the venture is a hobby — an activity not engaged in for profit — rather than a business. Then you’ll be unable to deduct losses.

By contrast, if the new enterprise isn’t affected by the hobby loss rules because it’s profitable, all otherwise allowable expenses are deductible on Schedule C, even if they exceed income from the enterprise.

Continue Reading

Adding a new partner in a partnership has several financial and legal implications. Let’s say you and your partners are planning to admit a new partner. The new partner will acquire a one-third interest in the partnership by making a cash contribution to it. Let’s further assume that your bases in your partnership interests are sufficient so that the decrease in your portions of the partnership’s liabilities because of the new partner’s entry won’t reduce your bases to zero.

Not as Simple as It Seems

Although the entry of a new partner appears to be a simple matter, it’s necessary to plan the new person’s entry properly in order to avoid various tax problems. Here are two issues to consider:

Continue Reading

The tax filing deadline for 2021 tax returns is April 18 this year. After your 2021 tax return has been successfully filed with the IRS, there may still be some issues to bear in mind. Here are three considerations:

1. You Can Throw Some Tax Records Away Now

You should hang onto tax records related to your return for as long as the IRS can audit your return or assess additional taxes. The statute of limitations is generally three years after you file your return. So you can generally get rid of most records related to tax returns for 2018 and earlier years. (If you filed an extension for your 2018 return, hold on to your records until at least three years from when you filed the extended return.)

Continue Reading

The federal government is helping to pick up the tab for certain business meals. Under a provision that’s part of one of the COVID-19 relief laws, the usual deduction for 50% of the cost of business meals is doubled to 100% for food and beverages provided by restaurants in 2022 (and 2021).

So, you can take a customer out for a business meal or order take-out for your team and temporarily write off the entire cost — including the tip, sales tax and any delivery charges.

Continue Reading

If you’re an investor in mutual funds or you’re interested in putting some money into them, you’re not alone. According to the Investment Company Institute, a survey found 58.7 million households owned mutual funds in mid-2020. But despite their popularity, the tax rules involved in selling mutual fund shares can be complex.

What Are the Basic Tax Rules?

Let’s say you sell appreciated mutual fund shares that you’ve owned for more than one year, the resulting profit will be a long-term capital gain. As such, the maximum federal income tax rate will be 20%, and you may also owe the 3.8% net investment income tax. However, most taxpayers will pay a tax rate of only 15%.

Continue Reading

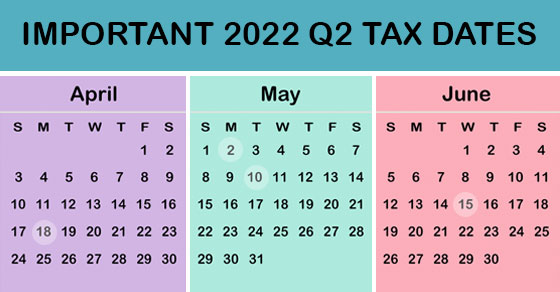

Here are some of the key tax-related deadlines that apply to businesses and other employers during the second quarter of 2022. Keep in mind that this list isn’t all-inclusive, so there may be additional deadlines that apply to you. Contact us to ensure you’re meeting all applicable deadlines and to learn more about the filing requirements.

Continue Reading

Summer is just around the corner. If you’re fortunate enough to own a vacation home, you may wonder about the tax consequences of renting it out for part of the year.

The tax treatment depends on how many days it’s rented and your level of personal use. Personal use includes vacation use by your relatives (even if you charge them market rate rent) and use by nonrelatives if a market rate rent isn’t charged.

Continue Reading

Typically, businesses want to delay recognition of taxable income into future years and accelerate deductions into the current year. But when is it prudent to do the opposite? And why would you want to?

One reason might be tax law changes that raise tax rates. There have been discussions in Washington about raising the corporate federal income tax rate from its current flat 21%. Another reason may be because you expect your noncorporate pass-through entity business to pay taxes at higher rates in the future, because the pass-through income will be taxed on your personal return. There have also been discussions in Washington about raising individual federal income tax rates.

Continue Reading

If your business doesn’t already have a retirement plan, now might be a good time to take the plunge. Current retirement plan rules allow for significant tax-deductible contributions.

For example, if you’re self-employed and set up a SEP-IRA, you can contribute up to 20% of your self-employment earnings, with a maximum contribution of $61,000 for 2022. If you’re employed by your own corporation, up to 25% of your salary can be contributed to your account, with a maximum contribution of $61,000. If you’re in the 32% federal income tax bracket, making a maximum contribution could cut what you owe Uncle Sam for 2022 by a whopping $19,520 (32% times $61,000).

Continue Reading