In today’s economy, many small businesses are strapped for cash. They may find it beneficial to barter or trade for goods and services instead of paying cash for them. Bartering is the oldest form of trade and the internet has made it easier to engage with other businesses. But if your business gets involved in bartering, be aware that the fair market value of goods that you receive in bartering is taxable income. And if you exchange services with another business, the transaction results in taxable income for both parties.

How It Works

Here are some examples:

- A computer consultant agrees to exchange services with an advertising agency.

- A plumber does repair work for a dentist in exchange for dental services.

Continue Reading

Despite the robust job market, there are still some people losing their jobs. If you’re laid off or terminated from employment, taxes are probably the last thing on your mind. However, there are tax implications due to your changed personal and professional circumstances. Depending on your situation, the tax aspects can be complex and require you to make decisions that may affect your tax picture this year and for years to come.

Unemployment and Severance Pay

Unemployment compensation is taxable, as are payments for any accumulated vacation or sick time. Although severance pay is also taxable and subject to federal income tax withholding, some elements of a severance package may be specially treated.

Continue Reading

If you’re getting ready to file your 2021 tax return, and your tax bill is more than you’d like, there might still be a way to lower it. If you’re eligible, you can make a deductible contribution to a traditional IRA right up until the April 18, 2022, filing date and benefit from the tax savings on your 2021 return.

Do You Qualify?

You can make a deductible contribution to a traditional IRA if:

- You (and your spouse) aren’t an active participant in an employer-sponsored retirement plan, or

- You (or your spouse) are an active participant in an employer plan, but your modified adjusted gross income (AGI) doesn’t exceed certain levels that vary from year-to-year by filing status.

Continue Reading

If you own your own company and travel for business, you may wonder whether you can deduct the costs of having your spouse accompany you on trips.

The rules for deducting a spouse’s travel costs are very restrictive. First of all, to qualify, your spouse must be your employee. This means you can’t deduct the travel costs of a spouse, even if his or her presence has a bona fide business purpose, unless the spouse is a bona fide employee of your business. This requirement prevents tax deductibility in most cases.

Continue Reading

If you made large gifts to your children, grandchildren or other heirs last year, it’s important to determine whether you’re required to file a 2021 gift tax return. And in some cases, even if it’s not required to file one, it may be beneficial to do so anyway.

Continue Reading

If you’re married, you may wonder whether you should file joint or separate tax returns. The answer depends on your individual tax situation.

In general, it depends on which filing status results in the lowest tax. But keep in mind that, if you and your spouse file a joint return, each of you is “jointly and severally” liable for the tax on your combined income. And you’re both equally liable for any additional tax the IRS assesses, plus interest and most penalties. That means that the IRS can come after either of you to collect the full amount.

Continue Reading

If you donated to charity last year, letters from the charities may have appeared in your mailbox recently acknowledging the donations. But what happens if you haven’t received such a letter — can you still claim a deduction for the gift on your 2021 income tax return? It depends.

The Requirements

To prove a charitable donation for which you claim a tax deduction, you need to comply with IRS substantiation requirements. For a donation of $250 or more, this includes obtaining a contemporaneous written acknowledgment from the charity stating the amount of the donation, whether you received any goods or services in consideration for the donation and the value of any such goods or services.

Continue Reading

Traditional IRAs and Roth IRAs have been around for decades and the rules surrounding them have changed many times. What hasn’t changed is that they can help you save for retirement on a tax-favored basis. Here’s an overview.

Traditional IRAs

You can make anannual deductible contribution to a traditional IRA if:

- You (and your spouse) aren’t active participants in employer-sponsored retirement plans, or

- You (or your spouse) are active participants in an employer plan, and your modified adjusted gross income (MAGI) doesn’t exceed certain levels that vary annually by filing status.

Continue Reading

If you’re in business for yourself as a sole proprietor, or you’re planning to start a business, you need to know about the tax aspects of your venture. Here are eight important issues to consider:

1. You report income and expenses on Schedule C of Form 1040. The net income is taxable to you regardless of whether you withdraw cash from the business. Your business expenses are deductible against gross income and not as itemized deductions. If you have any losses, they’re generally deductible against your other income, subject to special rules relating to hobby losses, passive activity losses and losses in activities in which you weren’t “at risk.”

Continue Reading

If you’re an employer with a business where tipping is customary for providing food and beverages, you may qualify for a federal tax credit involving the Social Security and Medicare (FICA) taxes that you pay on your employees’ tip income.

Basics of the Credit

The FICA credit applies with respect to tips that your employees receive from customers in connection with the provision of food or beverages, regardless of whether the food or beverages are for consumption on or off the premises. Although these tips are paid by customers, they’re treated for FICA tax purposes as if you paid them to your employees. Your employees are required to report their tips to you. You must withhold and remit the employee’s share of FICA taxes, and you must also pay the employer’s share of those taxes.

Continue Reading

While Congress didn’t pass the Build Back Better Act in 2021, there are still tax changes that may affect your tax situation for this year. That’s because some tax figures are adjusted annually for inflation.

If you’re like most people, you’re probably more concerned about your 2021 tax bill right now than you are about your 2022 tax situation. That’s understandable because your 2021 individual tax return is generally due to be filed by April 18 (unless you file an extension).

Continue Reading

Many tax limits that affect businesses are annually indexed for inflation, and a number of them have increased for 2022. Here’s a rundown of those that may be important to you and your business.

Social Security Tax

The amount of an employee’s earnings that is subject to Social Security tax is capped for 2022 at $147,000 (up from $142,800 in 2021).

Continue Reading

While some businesses have closed since the start of the COVID-19 crisis, many new ventures have launched. Entrepreneurs have cited a number of reasons why they decided to start a business in the midst of a pandemic. For example, they had more time, wanted to take advantage of new opportunities or they needed money due to being laid off. Whatever the reason, if you’ve recently started a new business, or you’re contemplating starting one, be aware of the tax implications.

As you know, before you even open the doors in a start-up business, you generally have to spend a lot of money. You may have to train workers and pay for rent, utilities, marketing and more.

Continue Reading

If you operate a business, or you’re starting a new one, you know you need to keep records of your income and expenses. Specifically, you should carefully record your expenses in order to claim all of the tax deductions to which you’re entitled. And you want to make sure you can defend the amounts reported on your tax returns in case you’re ever audited by the IRS.

Be aware that there’s no one way to keep business records. But there are strict rules when it comes to keeping records and proving expenses are legitimate for tax purposes. Certain types of expenses, such as automobile, travel, meals and home office costs, require special attention because they’re subject to special recordkeeping requirements or limitations.

Continue Reading

The IRS began accepting 2021 individual tax returns on January 24. If you haven’t prepared yet for tax season, here are three quick tips to help speed processing and avoid hassles.

Continue Reading

If you’re paying back college loans for yourself or your children, you may wonder if you can deduct the interest you pay on the loans. The answer is yes, subject to certain limits. The maximum amount of student loan interest you can deduct each year is $2,500. Unfortunately, the deduction is phased out if your adjusted gross income (AGI) exceeds certain levels, and as explained below, the levels aren’t very high.

The interest must be for a “qualified education loan,” which means a debt incurred to pay tuition, room and board, and related expenses to attend a post-high school educational institution, including certain vocational schools. Certain postgraduate programs also qualify. Therefore, an internship or residency program leading to a degree or certificate awarded by an institution of higher education, hospital or health care facility offering postgraduate training can qualify.

Continue Reading

The number of people engaged in the “gig” or sharing economy has grown in recent years. In an August 2021 survey, the Pew Research Center found that 16% of Americans have earned money at some time through online gig platforms. This includes providing car rides, shopping for groceries, walking dogs, performing household tasks, running errands and making deliveries from a restaurant or store.

There are tax consequences for the people who perform these jobs. Basically, if you receive income from an online platform offering goods and services, it’s generally taxable. That’s true even if the income comes from a side job and even if you don’t receive an income statement reporting the amount of money you made.

Continue Reading

Many employees — from retail workers to sales staffers involved in complex business-to-business transactions — receive part of their compensation from sales-related commissions. To attract and retain top talent, some companies even allow employees to earn unlimited commissions.

Unfortunately, some commission-compensated employees may be tempted to abuse this system by falsifying sales or rates. Fraud methods vary depending on an unethical salesperson’s employer and role. But companies need to be aware of the possibility of commission fraud and take steps to prevent it.

Continue Reading

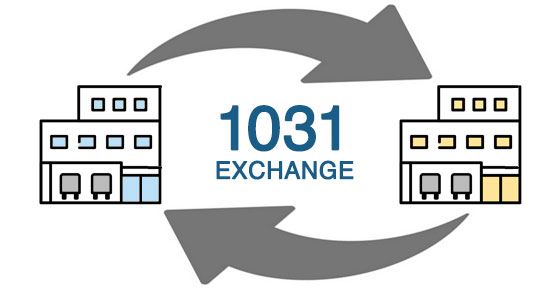

Do you want to sell commercial or investment real estate that has appreciated significantly? One way to defer a tax bill on the gain is with a Section 1031 “like-kind” exchange where you exchange the property rather than sell it. With real estate prices up in some markets (and higher resulting tax bills), the like-kind exchange strategy may be attractive.

A like-kind exchange is any exchange of real property held for investment or for productive use in your trade or business (relinquished property) for like-kind investment, trade or business real property (replacement property).

Continue Reading

After two years of no increases, the optional standard mileage rate used to calculate the deductible cost of operating an automobile for business will be going up in 2022 by 2.5 cents per mile. The IRS recently announced that the cents-per-mile rate for the business use of a car, van, pickup or panel truck will be 58.5 cents (up from 56 cents for 2021).

The increased tax deduction partly reflects the price of gasoline. On December 21, 2021, the national average price of a gallon of regular gas was $3.29, compared with $2.22 a year earlier, according to AAA Gas Prices.

Continue Reading

You may pay out a bundle in out-of-pocket medical costs each year. But can you deduct them on your tax return? It’s possible but not easy. Medical expenses can be claimed as a deduction only to the extent your unreimbursed costs exceed 7.5% of your adjusted gross income. Plus, medical expenses are deductible only if you itemize, which means that your itemized deductions must exceed your standard deduction.

Continue Reading

Awards and settlements are routinely provided for a variety of reasons. For example, a person could receive compensatory and punitive damage payments for personal injury, discrimination or harassment. Some of this money is taxed by the federal government, and perhaps state governments. Hopefully, you’ll never need to know how payments for personal injuries are taxed. But here are the basic rules — just in case you or a loved one does need to understand them.

Under tax law, individuals are permitted to exclude from gross income damages that are received on account of a personal physical injury or a physical sickness. It doesn’t matter if the compensation is from a court-ordered award or an out-of-court settlement, and it makes no difference if it’s paid in a lump sum or installments.

Continue Reading

The use of a company vehicle is a valuable fringe benefit for owners and employees of small businesses. This perk results in tax deductions for the employer as well as tax breaks for the owners and employees using the cars. (And of course, they get the nontax benefit of getting a company car.) Plus, current tax law and IRS rules make the benefit even better than it was in the past.

The Rules in Action

Let’s say you’re the owner-employee of a corporation that’s going to provide you with a company car. You need the car to visit customers, meet with vendors and check on suppliers. You expect to drive the car 8,500 miles a year for business. You also expect to use the car for about 7,000 miles of personal driving, including commuting, running errands and weekend trips. Therefore, your usage of the vehicle will be approximately 55% for business and 45% for personal purposes. You want a nice car to reflect positively on your business, so the corporation buys a new $55,000 luxury sedan.

Continue Reading

Year-end is a good time to plan to save taxes by carefully structuring your capital gains and losses.

Consider some possibilities if you have losses on certain investments to date. For example, suppose you lost money this year on some stock and have other stock that has appreciated. Consider selling appreciated assets before December 31 (if you think their value has peaked) and offsetting gains with losses.

Continue Reading

Here are some of the key tax-related deadlines affecting businesses and other employers during the first quarter of 2022. Keep in mind that this list isn’t all-inclusive, so there may be additional deadlines that apply to you. Contact us to ensure you’re meeting all applicable deadlines and to learn more about the filing requirements.

Continue Reading

Don’t let the holiday rush keep you from considering some important steps to reduce your 2021 tax liability. You still have time to execute a few strategies.

Purchase Assets

Thinking about buying new or used equipment, machinery or office equipment in the new year? Buy them and place them in service by December 31, and you can deduct 100% of the cost as bonus depreciation. Contact us for details on the 100% bonus depreciation break and exactly what types of assets qualify.

Continue Reading

If you’re starting to worry about your 2021 tax bill, there’s good news — you may still have time to reduce your liability. Here are three quick strategies that may help you trim your taxes before year-end.

Continue Reading

With the increasing cost of employee health care benefits, your business may be interested in providing some of these benefits through an employer-sponsored Health Savings Account (HSA).

For eligible individuals, an HSA offers a tax-advantaged way to set aside funds (or have their employers do so) to meet future medical needs. Here are the important tax benefits:

- Contributions that participants make to an HSA are deductible, within limits.

- Contributions that employers make aren’t taxed to participants.

- Earnings on the funds in an HSA aren’t taxed, so the money can accumulate tax free year after year.

- Distributions from HSAs to cover qualified medical expenses aren’t taxed.

- Employers don’t have to pay payroll taxes on HSA contributions made by employees through payroll deductions.

Continue Reading

The Infrastructure Investment and Jobs Act (IIJA) was signed into law on November 15, 2021. It includes new information reporting requirements that will generally apply to digital asset transactions starting in 2023. Cryptocurrency exchanges will be required to perform intermediary Form 1099 reporting for cryptocurrency transactions.

Existing Reporting Rules

If you have a stock brokerage account, whenever you sell stock or other securities, you receive a Form 1099-B after the end of the year. Your broker uses the form to report transaction details such as sale proceeds, relevant dates, your tax basis and the character of gains or losses. In addition, if you transfer stock from one broker to another broker, the old broker must furnish a statement with relevant information, such as tax basis, to the new broker.

Continue Reading

Are you planning to launch a business or thinking about changing your business entity? If so, you need to determine which entity will work best for you — a C corporation or a pass-through entity such as a sole-proprietorship, partnership, limited liability company (LLC) or S corporation. There are many factors to consider and proposed federal tax law changes being considered by Congress may affect your decision.

The corporate federal income tax is currently imposed at a flat 21% rate, while the current individual federal income tax rates begin at 10% and go up to 37%. The difference in rates can be mitigated by the qualified business income (QBI) deduction that’s available to eligible pass-through entity owners that are individuals, estates and trusts.

Continue Reading