Retirement is often viewed as an opportunity to travel, spend time with family or simply enjoy the fruits of a long career. Yet the transition may bring a tangle of tax considerations. Planning carefully can help you minimize tax bills. Below are four steps to take if you’re approaching retirement, along with the tax implications.

1. Consider Your Post-career Lifestyle

Begin by assessing what retirement might look like for you. For example, will you relocate to a different state or downsize by selling your home? Will you continue to work part-time?

Continue Reading

Chances are, you’re more concerned about your 2024 tax return right now than you are about your 2025 tax situation. That’s understandable because your 2024 individual tax return is due to be filed by April 15 (unless you file for an extension).

However, it’s a good time to familiarize yourself with tax amounts that may have changed for 2025 due to inflation. Not all tax figures are adjusted annually for inflation, and some amounts only change when Congress passes new laws.

Continue Reading

The nationwide price of gas is slightly higher than it was a year ago and the 2025 optional standard mileage rate used to calculate the deductible cost of operating an automobile for business has also gone up. The IRS recently announced that the 2025 cents-per-mile rate for the business use of a car, van, pickup or panel truck is 70 cents. In 2024, the business cents-per-mile rate was 67 cents per mile. This rate applies to gasoline and diesel-powered vehicles as well as electric and hybrid-electric vehicles.

The process of calculating rates

The 3-cent increase from the 2024 rate goes along with the recent price of gas. On January 17, 2025, the national average price of a gallon of regular gas was $3.11, compared with $3.08 a year earlier, according to AAA Fuel Prices. However, the standard mileage rate is calculated based on all the costs involved in driving a vehicle — not just the price of gas.

Continue Reading

The IRS announced it will start the 2025 filing season for individual income tax returns on January 27. That’s when the agency began accepting and processing 2024 tax year returns. Even if you typically don’t file until much closer to the mid-April deadline (or you file for an extension), you may want to file earlier this year. The reason is you can potentially protect yourself from tax identity theft.

Here are some answers to questions taxpayers may have about filing.

Continue Reading

Once you reach age 73, tax law requires you to begin taking withdrawals — called Required Minimum Distributions (RMDs) — from your traditional IRA, SIMPLE IRA and SEP IRA. Since funds can’t stay in these accounts indefinitely, it’s important to understand the rules behind RMDs, which can be pretty complex. Below, we address some common questions to help you navigate this process.

What Are the Tax Implications if I Want to Withdraw Money Before Retirement?

If you need to take money out of a traditional IRA before age 59½, distributions are taxable, and you may be subject to a 10% penalty tax. However, there are several ways that you can avoid the 10% penalty tax (but not the regular income tax). They include using the money to pay:

- Qualified higher education expenses,

- Up to $10,000 of expenses if you’re a first-time homebuyer,

- Expenses after you become totally and permanently disabled,

- Expenses of up to $5,000 per child for qualified birth or adoption expenses, and

- Health insurance premiums while unemployed.

Continue Reading

There are two tax breaks that help eligible parents offset the expenses of adopting a child. In 2025, adoptive parents may be able to claim a credit against their federal tax for up to $17,280 of “qualified adoption expenses” for each child. This is up from $16,810 in 2024. A tax credit is a dollar-for-dollar reduction of tax.

Also, adoptive parents may be able to exclude from an employee’s gross income up to $17,280 in 2025 ($16,810 in 2024) of qualified expenses paid by an employer under an adoption assistance program. Both the credit and the exclusion are phased out if the parents’ income exceeds certain limits detailed below.

Continue Reading

When deciding on the best structure for your business, one option to consider is a C corporation. This entity offers several advantages and disadvantages that may significantly affect your business operations and financial health. Here’s a detailed look at the pros and cons of operating as a C corporation.

Tax Implications

A C corporation allows the business to be treated and taxed separately from you as the principal owner. The corporate tax rate is currently 21%, which is lower than the highest noncorporate tax rate of 37%.

Continue Reading

When considering the advantages of U.S. Treasury savings bonds, you may appreciate their relative safety, simplicity and government backing. However, like all interest-bearing investments, savings bonds come with tax implications that are important to understand.

Deferred Interest

Series EE Bonds dated May 2005 and after earn a fixed rate of interest. Bonds purchased between May 1997 and April 30, 2005, earn a variable market-based rate of return.

Continue Reading

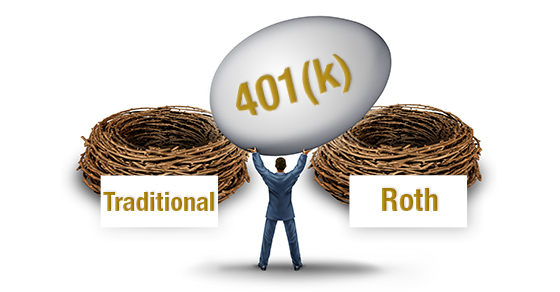

Saving for retirement is a crucial financial goal and a 401(k) plan is one of the most effective tools for achieving it. If your employer offers a 401(k) or Roth 401(k), contributing as much as possible to the plan in 2025 is a smart way to build a considerable nest egg.

If you’re not already contributing the maximum allowed, consider increasing your contribution in 2025. Because of tax-deferred compounding (tax-free in the case of Roth accounts), boosting contributions can have a significant impact on the amount of money you’ll have in retirement.

Continue Reading

As higher education costs continue to rise, you may be concerned about how to save and pay for college. Fortunately, several tools and strategies offered in the U.S. tax code may help ease the financial burden. Below is an overview of some of the most beneficial tax breaks and planning options for funding your child’s or grandchild’s education.

Qualified Tuition Programs or 529 Plans

A 529 plan allows you to buy tuition credits or contribute to an account set up to meet your child’s future higher education expenses. State governments or private institutions establish 529 plans.

Continue Reading

Intangible assets, such as patents, trademarks, copyrights and goodwill, play a crucial role in today’s businesses. The tax treatment of these assets can be complex, but businesses need to understand the issues involved. Here are some answers to frequently asked questions.

What Are Intangible Assets?

The term “intangibles” covers many items. Determining whether an acquired or created asset or benefit is intangible isn’t always easy. Intangibles include debt instruments, prepaid expenses, non-functional currencies, financial derivatives (including, but not limited to, options, forward or futures contracts, and foreign currency contracts), leases, licenses, memberships, patents, copyrights, franchises, trademarks, trade names, goodwill, annuity contracts, insurance contracts, endowment contracts, customer lists, ownership interests in any business entities (for example, corporations, partnerships, LLCs, trusts and estates) and other rights, assets, instruments and agreements.

Continue Reading

If you’ve reached age 70½, you can make cash donations directly from your IRA to IRS-approved charities. These qualified charitable distributions (QCDs) may help you gain tax advantages.

QCD Basics

QCDs can be made from your traditional IRA(s) free of federal income tax. In contrast, other traditional IRA distributions are wholly or partially taxable, depending on whether you’ve made nondeductible contributions over the years.

Continue Reading

As a small business owner, managing health care costs for yourself and your employees can be challenging. One effective tool to consider adding is a Health Savings Account (HSA). HSAs offer a range of benefits that can help you save on health care expenses while providing valuable tax advantages. You may already have an HSA. It’s a good time to review how these accounts work because the IRS has announced the relevant inflation-adjusted amounts for 2025.

HSA Basics

For eligible individuals, HSAs offer a tax-advantaged way to set aside funds (or have their employers do so) to meet future medical needs. Employees can’t be enrolled in Medicare or claimed on someone else’s tax return.

Continue Reading

Inflation can have a significant impact on federal tax breaks. While recent inflation has come down since its peak in 2022, some tax amounts will still increase for 2025. The IRS recently announced next year’s inflation-adjusted amounts for several provisions.

Here are the highlights.

Continue Reading

You’re not alone if you’re confused about the federal tax treatment of business-related meal and entertainment expenses. The rules have changed in recent years. Let’s take a look at what you can deduct in 2024.

Current Law

The Tax Cuts and Jobs Act eliminated deductions for most business-related entertainment expenses. That means, for example, that you can’t deduct any part of the cost of taking clients out for a round of golf or to a football game.

Continue Reading

If you own a growing, unincorporated small business, you may be concerned about high self-employment (SE) tax bills. The SE tax is how Social Security and Medicare taxes are collected from self-employed individuals like you.

SE Tax Basics

The maximum 15.3% SE tax rate hits the first $168,600 of your 2024 net SE income. The 15.3% rate is comprised of the 12.4% rate for the Social Security tax component plus the 2.9% rate for the Medicare tax component. For 2025, the maximum 15.3% SE tax rate will hit the first $176,100 of your net SE income.

Continue Reading

Employee stock options remain a potentially valuable asset for employees who receive them. For example, many Silicon Valley millionaires got rich (or semi-rich) from exercising stock options when they worked for start-up companies or fast-growing enterprises.

We’ll explain what you need to know about the federal income and employment tax rules for employer-issued nonqualified stock options (NQSOs).

Continue Reading

How much can you and your employees contribute to your 401(k)s or other retirement plans next year? In Notice 2024-80, the IRS recently announced cost-of-living adjustments that apply to the dollar limitations for retirement plans, as well as other qualified plans, for 2025. With inflation easing, the amounts aren’t increasing as much as in recent years.

401(k) Plans

The 2025 contribution limit for employees who participate in 401(k) plans will increase to $23,500 (up from $23,000 in 2024). This contribution amount also applies to 403(b) plans, most 457 plans and the federal government’s Thrift Savings Plan.

Continue Reading

Hiring household help, whether you employ a nanny, housekeeper or gardener, can significantly ease the burden of childcare and daily chores. However, as a household employer, it’s critical to understand your tax obligations, commonly called the “nanny tax.” If you hire a household employee who isn’t an independent contractor, you may be liable for federal income tax and other taxes (including state tax obligations).

If you employ a household worker, you aren’t required to withhold federal income taxes from pay. But you can choose to withhold if the worker requests it. In that case, ask the worker to fill out a Form W-4. However, you may be required to withhold Social Security and Medicare (FICA) taxes and to pay federal unemployment (FUTA) tax.

Continue Reading

As a business owner, you may travel to visit customers, attend conferences, check on vendors and for other purposes. Understanding which travel expenses are tax deductible can significantly affect your bottom line. Properly managing travel costs can help ensure compliance and maximize your tax savings.

Your Tax Home

Eligible taxpayers can deduct the ordinary and necessary expenses of business travel when away from their “tax homes.” Ordinary means common and accepted in the industry. Necessary means helpful and appropriate for the business. Expenses aren’t deductible if they’re for personal purposes, lavish or extravagant. That doesn’t mean you can’t fly first class or stay in luxury hotels. But you’ll need to show that expenses were reasonable.

Continue Reading

With the arrival of fall, it’s an ideal time to begin implementing strategies that could reduce your tax burden for both this year and next.

One of the first planning steps is to ascertain whether you’ll take the standard deduction or itemize deductions for 2024. You may not itemize because of the high 2024 standard deduction amounts ($29,200 for joint filers, $14,600 for singles and married couples filing separately, and $21,900 for heads of household). Also, many itemized deductions have been reduced or suspended under current law.

Continue Reading

If you own a small business with no employees (other than your spouse) and want to set up a retirement plan, consider a solo 401(k) plan. This is also an option for self-employed individuals or business owners who wish to upgrade from a SIMPLE IRA or Simplified Employee Pension (SEP) plan.

A solo 401(k), also known as an individual 401(k), may offer advantages in terms of contributions, tax savings and investment options. These accounts are geared toward self-employed individuals, including sole proprietors, owners of single-member limited liability companies, consultants and other one-person businesses.

Continue Reading

As we approach 2025, changes are coming to the Social Security wage base. The Social Security Administration recently announced that the wage base for computing Social Security tax will increase to $176,100 for 2025 (up from $168,600 for 2024). Wages and self-employment income above this amount aren’t subject to Social Security tax.

If your business has employees, you may need to budget for additional payroll costs, especially if you have many high earners.

Continue Reading

Does your business require real estate for its operations? Or do you hold property titled under your business’s name? It might be worth reconsidering this strategy. With long-term tax, liability and estate planning advantages, separating real estate ownership from the business may be a wise choice.

How Taxes Affect a Sale

Businesses that are formed as C corporations treat real estate assets as they do equipment, inventory and other business assets. Any expenses related to owning the assets appear as ordinary expenses on their income statements and are generally tax deductible in the year they’re incurred.

Continue Reading

As the end of the year approaches, many people start to think about their finances and tax strategies. One effective way to reduce potential estate taxes and show generosity to loved ones is by giving cash gifts before December 31. Under tax law, you can gift a certain amount each year without incurring gift taxes or requiring a gift tax return. Taking advantage of this rule can help you reduce the size of your taxable estate while benefiting your family and friends.

Taxpayers can transfer substantial amounts, free of gift taxes, to their children or other recipients each year through the proper use of the annual exclusion. The exclusion amount is adjusted for inflation annually, and in 2024 is $18,000. It covers gifts that an individual makes to each recipient each year. So a taxpayer with three children can transfer $54,000 ($18,000 × 3) to the children this year, free of federal gift taxes. If the only gifts during a year are made this way, there’s no need to file a federal gift tax return. If annual gifts exceed $18,000 per recipient, the exclusion covers the first $18,000 and only the excess is taxable.

Continue Reading

If you have a child or grandchild planning to attend college, you’ve probably heard about qualified tuition programs, also known as 529 plans. These plans, named for the Internal Revenue Code section that provides for them, allow prepayment of higher education costs on a tax-favored basis.

There are two types of programs:

- Prepaid plans, which allow you to buy tuition credits or certificates at present tuition rates, even though the beneficiary (child) won’t be starting college for some time; and

- Savings plans, which depend on the performance of the fund(s) you invest your contributions in.

Continue Reading

The IRS has been increasing its audit efforts, focusing on large businesses and high-income individuals. By 2026, it plans to nearly triple its audit rates for large corporations with assets exceeding $250 million. Under these plans, partnerships with assets over $10 million will also see audit rates increase tenfold by 2026. This ramp-up in audits is part of the IRS’s broader strategy, funded by the Inflation Reduction Act, to target wealthier entities and high-dollar noncompliance.

The IRS doesn’t plan to increase audits for individuals making less than $400,000 annually. Small businesses are also unlikely to see a rise in audit rates in the near future, as the IRS is prioritizing more complex returns for higher-wealth entities. For example, the tax agency has announced that one focus area is taxpayers who personally use business aircraft. A business can deduct the cost of purchasing and using corporate planes, but personal trips, including vacation travel, aren’t deductible.

Continue Reading

Let’s say you have an unincorporated sideline activity that you consider a business. Perhaps you offer photography services, create custom artwork or sell handmade items online. Will the IRS agree that your venture is a business, not a hobby? It’s an essential question for tax purposes.

If the expenses from an activity exceed the revenues, you have a net loss. You may think you can deduct that loss on your personal federal income tax return with no questions asked. Not so fast! The IRS often claims that money-losing sidelines are hobbies rather than businesses — and the federal income tax rules for hobbies aren’t in your favor.

Continue Reading

The recent drop in interest rates has created a buzz in the real estate market. Potential homebuyers may now have an opportunity to attain their dreams of purchasing property. “The recent development of lower mortgage rates coupled with increasing inventory is a powerful combination that will provide the environment for sales to move higher in future months,” said National Association of Realtors Chief Economist Lawrence Yun.

If you’re in the process of buying a home, or you just bought one, you may wonder if you can deduct mortgage points paid on your behalf by the seller. The answer is “yes,” subject to some significant limitations described below.

Continue Reading

Employee health coverage is a significant part of many companies’ benefits packages. However, the administrative responsibilities that accompany offering health insurance can be complex. One crucial aspect is understanding the reporting requirements of federal agencies such as the IRS. Does your business have to comply, and if so, what must you do? Here are some answers to questions you may have.

What Is the Number of Employees Before Compliance Is Required?

The Affordable Care Act (ACA), enacted in 2010, introduced several employer responsibilities regarding health coverage. Certain employers with 50 or more full-time employees (called “applicable large employers” or ALEs) must use Forms 1094-C and 1095-C to report information about health coverage offers and enrollment for their employees.

Continue Reading